When it comes to the „VAT gap”, the Romanian Government and the European Commission have different views on the elements contributing to this indicator. Even different definitions.

When it comes to the „VAT gap”, the Romanian Government and the European Commission have different views on the elements contributing to this indicator. Even different definitions.

The difference between the Government’s approach and the Commission’s approach sets out two versions, both having an impact on the business environment, which is required to apply the split VAT:

either the split VAT payment applied by the companies working openly is a new pretext for the Government to avoid looking at the really damaging areas for the budget;

or this is a diversion set by the Government to preserve the evasion areas from which political parties are usually financed.

Here are the differences of approach and the definition:

1-. The Romanian Government officially admits that the VAT gap in 2015 – that is, the „difference between the VAT declared and the VAT collected” – is about RON 14 billion (about EUR 3 billion).

2-. The European Commission, in its most recent report, published in September, mentions a VAT gap of EUR 7.6 billion for Romania.

Where does the difference come from?

From the elements considered. While the Government looks at the VAT from the companies’ tax statements, the Commission looks at (many) more elements: specifically, those that leave Romania’s budget without collected VAT.

Bucharest and Brussels know different definitions of VAT gap

- Romanian Government’s definition:

On August 30, 2017, Tudose government issues three government ordinances that amend the Tax Code, the change with the greatest impact on the business environment being the decision on the split VAT payment.

In the explanatory memorandum, the Government says the measure is a reaction to the fact that Romania ranks the last in Europe in terms of the VAT gap.

In the same official document, the Government also offers its own definition of the term:

„The VAT gap is defined as the difference between the amount of VAT collected and the total VAT that should have been collected and is expressed in both absolute and relative terms. The total VAT that should be collected is the theoretical tax liability according to the tax legislation.”

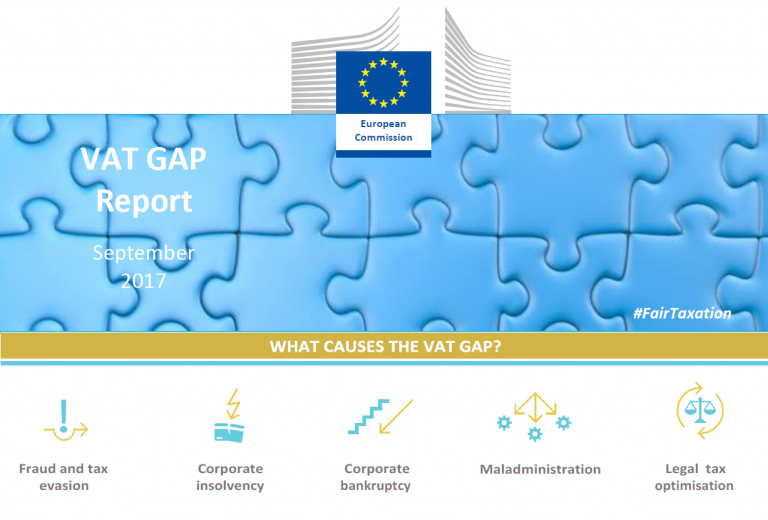

2 -Definition of the European Commission: five elements taken into account, most of them ignored by the Government:

The European Commission, in its most recent report on VAT gap, has a completely different definition of the term.

In Brussels, the answer to the question: „What does the VAT gap produce?” has the following answer:

In Brussels, the answer to the question: „What does the VAT gap produce?” has the following answer:

1- Fraud and tax evasion

2- Insolvency

3- Bankruptcy

4 – Poor administration

5- Tax optimizations

How many of the five „sources of VAT gap” does the Government ignore, before rushing into firms that operate openly and state their VAT?

What does it hide behind split VAT

Government’s official communication insists on the idea that the decision on split VAT payments will increase tax compliance.

The problem is that the very definition offered by the Government for the VAT gap shows that the tax authority is not concerned enough about its core mission – prevention, guidance and control.

That is because we are talking about taxpayers that declared taxes but have not paid them anymore. Reasons for non-payment may be different.

It cannot be understood, though, how the Finance Ministry says they missed to collect EUR 3 billion from VAT in 2015, in the context in which most companies in Romania receive, barely two weeks after the 25th of the month, the orders for payment procedure and the decision for the attachment of their bank accounts.

Perhaps this rule does not apply to everyone, maybe there are companies about which ANAF has not been concerned for years, allowing them to operate freely without paying taxes.

Perhaps state-owned companies are not controlled, perhaps they are „strategic” companies, maybe the fault lies with the insufficient development of the technical infrastructure of the tax authority.

It is certainly not the fault of those who declare taxes and pay them on time, correctly or with a delay but with penalties and interest applied.

On the real causes of the VAT gap (the real gap, not the one created in Bucharest, ignoring the big sources for the budget damage), cursdeguvernare.ro will get back in a future edition.