Hourly labour costs grew by 13.09% in the fourth quarter of 2018 compared to the same period in 2017, according to data announced by INS. This rhythm is in a slight decline compared to 13.91% recorded in the previous quarter, but above the threshold of 12% set by the European macroeconomic stability requirements, a situation perpetuated since Q4 2016.

Hourly labour costs grew by 13.09% in the fourth quarter of 2018 compared to the same period in 2017, according to data announced by INS. This rhythm is in a slight decline compared to 13.91% recorded in the previous quarter, but above the threshold of 12% set by the European macroeconomic stability requirements, a situation perpetuated since Q4 2016.

Moreover, while at the end of last year the increase in labour cost was about double compared to GDP growth (estimated at 7%), in the last quarter of 2018, a ratio more than triple has been reached, amid the slowdown in the economic growth to just over four percentage points.

An increasing discrepancy between the two indicators raises questions

*

- Hourly labour cost evolution

- (Q4 2016- Q4 2018, % compared to the same quarter of the previous year)

- Quarter

- Hourly labour cost

- Quarter

- Hourly labour cost

*

And that was before new salary increases came into force, arbitrarily stipulated in a systematic growth pay scale committed for 2022, without the certainty that the growth forecast (already in distress) will be achieved. Practically, the steady growth trend in labour costs generates inflationary pressures and reduces competitiveness.

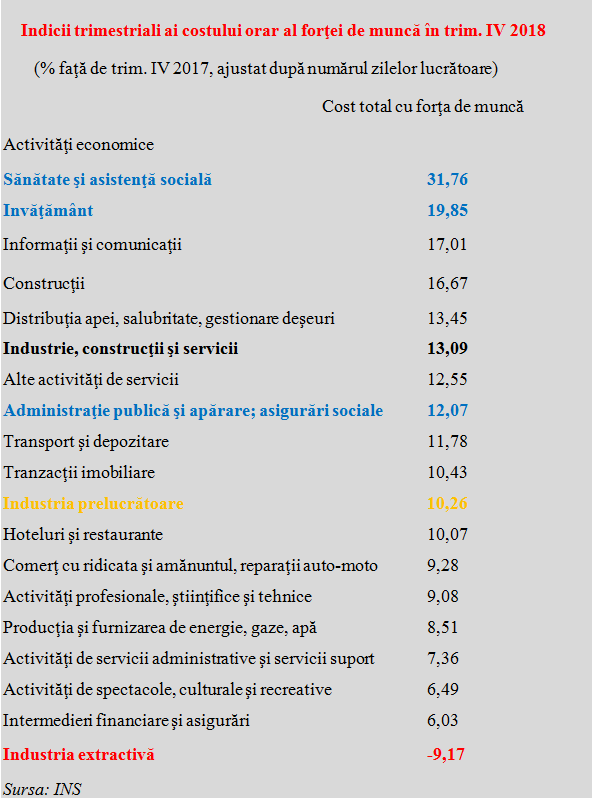

In the structure by economic fields, there are significant differences in wage evolution, from an increase of more than 30% in health (sent directly to the 2022 pay scale) to a nearly ten percentage point decrease in the mining field.

We present how the labour cost in different fields of the economy, defined according to international norms (see table), has evolved over the past 12 months.

*

- Quarterly indices of hourly labour cost in Q4 2018

- (% compared to Q4 2017, adjusted based on the number of working days)

- Total labour cost

- Economic activities

- Health and social assistance

- Education

- IT&C

- Construction

- Water supply, sanitation and waste management

- Manufacturing, construction and services

- Other service activities

- Public administration and defence; social insurance

- Transport and warehousing

- Real estate

- Manufacturing

- Hotels and restaurants

- Retail and wholesale trade, auto repairs

- Professional, scientific and technical activities

- Energy, gas and water production and supply

- Administrative and support service activities

- Entertainment, cultural and leisure activities

- Financial intermediation and insurance

- Extractive industry

*

The public sector has already positioned significantly above the average in the economy, with health and education holding the first two positions in the increases ranking. However, it should be noted that „Public administration and defence; social insurance” segment is positioned slightly below the industry, construction and services group, which is an evolution worth to be welcomed.

Unfortunately, the manufacturing industry, which gives the overall tone in the economy, remained in the second half of the ranking. However, the unbalance between the „real” economy and the steady rise in wages from the public sector (which reached somewhere around the 10% of GDP threshold) and pensions (which will increase significantly during the electoral period at the end of the year) will pose major problems in terms of financing.

We remind that two-digit wage increases are rare in a settled economy. The share of wages in the cost of products has already led, by way of salary increases, to an advance of about four percentage points in industrial production prices. An advance that will have to be integrated into the commercial chain and is already seen at the shelf.

As far as the labour productivity is concerned, which should be above salary increases, in optimal theoretical terms, better performance in 2017 attenuated in 2018, and official data does not look very good if we relate to the wage advance of more than four times the measured results.

*

- Labour productivity in manufacturing

- Year

- Labour productivity

*

That is why it would be important for 2019 to achieve a more pronounced increase in labour productivity while limiting the wage growth rate to acceptable levels.

A level slightly higher than the economic growth is possible given that the share of labour remuneration in GDP is still relatively low, but forcing the growth in an area competitive environment is not recommended.