Gross Domestic Product for the first quarter of 2019 increased by 5% in real terms compared to the same period of the previous year (5.1% adjusted by seasonality, which will be communicated to Eurostat for comparability with other EU member states).

Gross Domestic Product for the first quarter of 2019 increased by 5% in real terms compared to the same period of the previous year (5.1% adjusted by seasonality, which will be communicated to Eurostat for comparability with other EU member states).

According to the same INS „signal” release, the advance compared to the previous quarter was 1.3% (seasonally adjusted as well).

The official gross commercial result is above expectations and better than in the four quarters of last year, although the advance of the main component that influences the advance of the gross value added, the manufacturing sector, declined to just 1.2% in Q1 2019 compared to 5.9% in Q1 2018.

Explanations on the structure of GDP formation will come in the next release, in the provisional version of recording the economic growth.

*

- Evolution of quarterly GDP compared to the same quarter of the previous year (%, gross series)

- Quarter

*

The rather high growth rate relative to the previous quarter, about four times higher than in the same period of Q1 2018, should correspond to a net higher economic growth at the beginning of this year compared to the beginning of last year. An advance that is found neither in the manufacturing sector nor in the moderate growth of the private sector, where the segment of self-employed professionals was in decline.

*

- Evolution of quarterly GDP compared to the previous quarter (%, seasonally adjusted series)

- Quarter

*

Noteworthy, the share of the first quarter in the overall result of a year is relatively low, somewhere around 20% instead of 25%, as it would have been in the case of evenly distributed results over all four quarters of the year. A simple mathematical equation shows that we shall need an even higher average growth rate, of 5.6% in the remaining three quarters, in order to achieve the level of 5.5% officially predicted by the National Commission for Strategy and Prognosis.

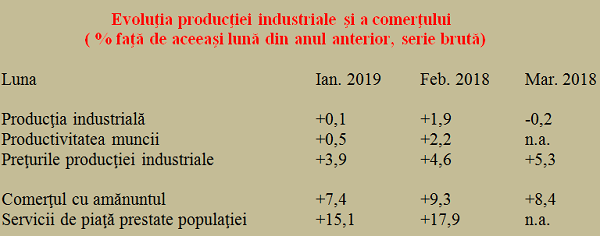

Unfortunately, industrial production growth rate, which supports the entire economy, has been quite weak since the beginning of the year and even declining in March. It is noteworthy that, in the context of a price increasing trend in this sector, which will translate into a deflator (equivalent to the inflation in the whole economy, not just for the population), which will tend to reduce, in real terms, the economic growth recorded in current prices.

*

- Evolution of manufacturing production and trade (% compared to the same quarter of the previous year, gross series)

- Month Jan 2019 Feb 2018 March 2018

- Industrial production

- Labour productivity

- Prices in industrial production

- Retail

- Market services provided to the population

*

If we correlate with the modest increase in labour productivity, the explanation for the increasing GDP growth rate seems to come rather from the evolution in the retail and services provided to the population, inflated up to values far above the results in the manufacturing sector.

The result of +12.5% in the construction sector is exceptional, but given its relatively small share of GDP, it cannot explain the increasing economic advance. We shall see that in the presentation of the economic growth structure on Q1 2019 but until then we should pay attention to the vertiginous increase in the balance of payments deficit right on the goods and services segment.